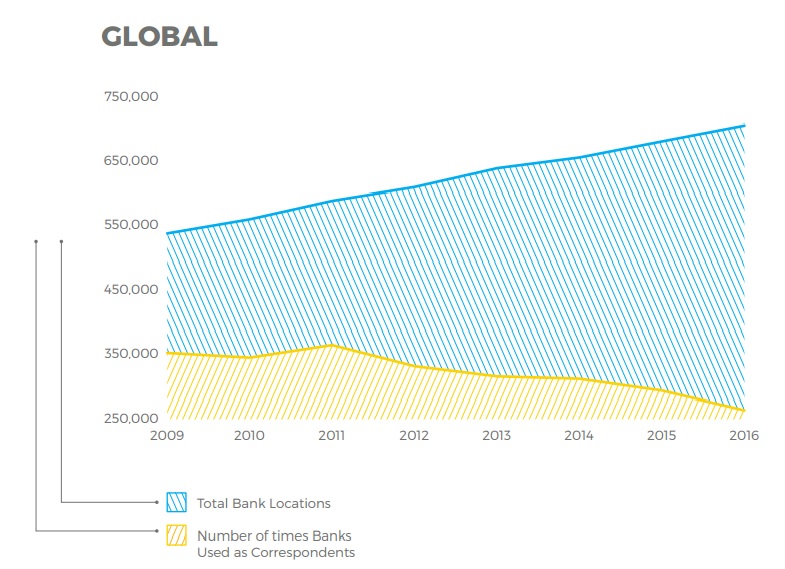

Recent correspondent banking research has revealed that between 2009 and 2016, correspondent banking relationships, where one financial institution provides services on behalf of another in a different location to facilitate cross-border payments, have reduced globally by 25%.

This comes despite the fact that global GDP per capita grew during the same period, following the 2008 financial crisis.

Commenting on the findings, Henry Balani, Global Head of Strategic Affairs at Accuity, the research provider said, “Correspondent banking represents the cornerstone of the global payment system designed to serve the settlement of financial transactions across country borders. Our Research highlights some important trends in de-risking and its impact on international trade and global banking.

“The irony is that regulation designed to protect the global financial system is, in a sense, having an opposite effect and forcing whole regions outside the regulated financial system. This matters because allowing de-risking to continue unfettered is like living in a world where some airports don’t have the same levels of security screening – before long, the consequences will be disastrous for everyone.”

Measuring the cost of global de-risking

Since the global financial crisis of 2008, regulators have imposed requirements for greater transparency, established higher liquidity thresholds for banks as well as stepping up enforcement actions on institutions that violate anti-money laundering (AML) regulations.

In 2014, AML penalties peaked at $10 billion compounding the challenges banks face in high-risk geographies. In this climate, the threat to banks of doing business in these geographies potentially outweighs the benefits of services to their clients, even if there may be good business opportunities to pursue.

The challenges of increased operational costs, competitive and regulatory pressures have driven banks to withdraw from correspondent banking relationships. Historically, these relationships were provided as services to international customers, but this is no longer viable, as banks cannot justify the increased compliance cost associated with offering correspondent banking services to their local customers.

As a result, businesses in the regions most affected are struggling to access the global financial systems to finance their operations. Without this access, local banks are forced to use non-regulated, higher cost sources of finance and expose themselves to nefarious actors and shadow banking.

Henry Balani added: “A number of factors have contributed to derisking, the most important being that the risk / reward balance has become unfavourable for large clearing banks and in response they have taken a country / region risk view in deciding who they can do business with. If we want to reverse this trend and begin to ‘re-risk’, then the ‘antidote’ will require more granular level due diligence and proper risk assessments to provide large clearers with the confidence that they can deal with low risk businesses in high risk jurisdictions.”

Decline in USD relationships is either indicative of a concentration in relationships or a reduction in USD dominance

- The number of USD correspondent relationships declined by 15% with Euro relationships showing a steeper decline of 23%

- The number of Chinese Renminbi (RMB) correspondent relationships increased by 8%

- Global bank locations in developing economies increased by 31% since 2014

Findings from this research reflect the number of correspondent banking relationships transacting in particular currencies rather than the volume of currency transactions. Research shows a steady decline in the number of USD correspondent banking relationships globally since 2014. The USD was the currency of choice as the global economy recovered from the global financial crisis in 2008. While USD continues to be the currency of choice, the rate of decline in the number of USD relationships further accelerated with a drop of 13% between 2015 and 2016 from a decline of 2% between 2014 and 2015.

While the 25% drop in global correspondent relationships is greater than the USD correspondents decline, the trend for USD is particularly significant when compared to the contrarian increase in the number of Chinese RMB correspondent banking relationships. Since 2014, research shows an 8% increase and since 2012, the number of the RMB relationships showed a dramatic increase from 3,600 to 8,800 relationships in 2016 (albeit from a low base). The research further reveals a peak in the number of RMB correspondent banking relationships in 2015 as the USD continued to decline.

There are two explanations for this decline in USD relationships when compared to the RMB. Either there is a concentration in USD relationships, with more transactions settled through fewer relationships, or there is a decline in the dominance of USD.

Global bank locations in developing economies have also increased by 31% since 2014, largely due to growth in China and APAC. This is significant as the number of banks in established global financial centers are in decline.